A budget gives us a clear picture of how much money we have coming in each week or month, and how much we can spend. It can also help us to save for the future, deal with unexpected costs and take control of debt.

If you own a business, it is good practice to develop separate budgets for household and business income and expenditure. Decide how much business money should be classed as wages for you and any other family members, and include these wages in the household budget.

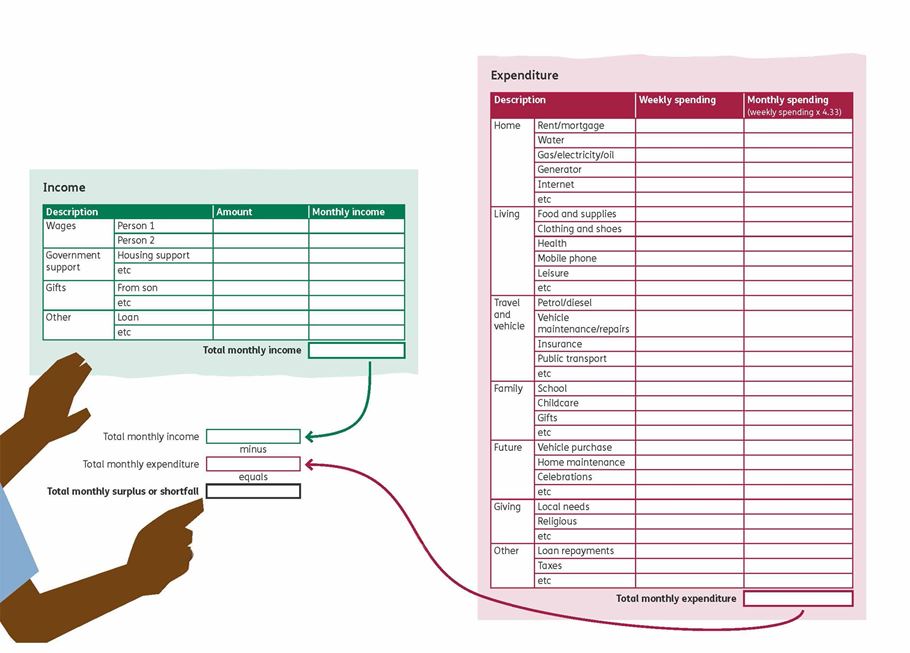

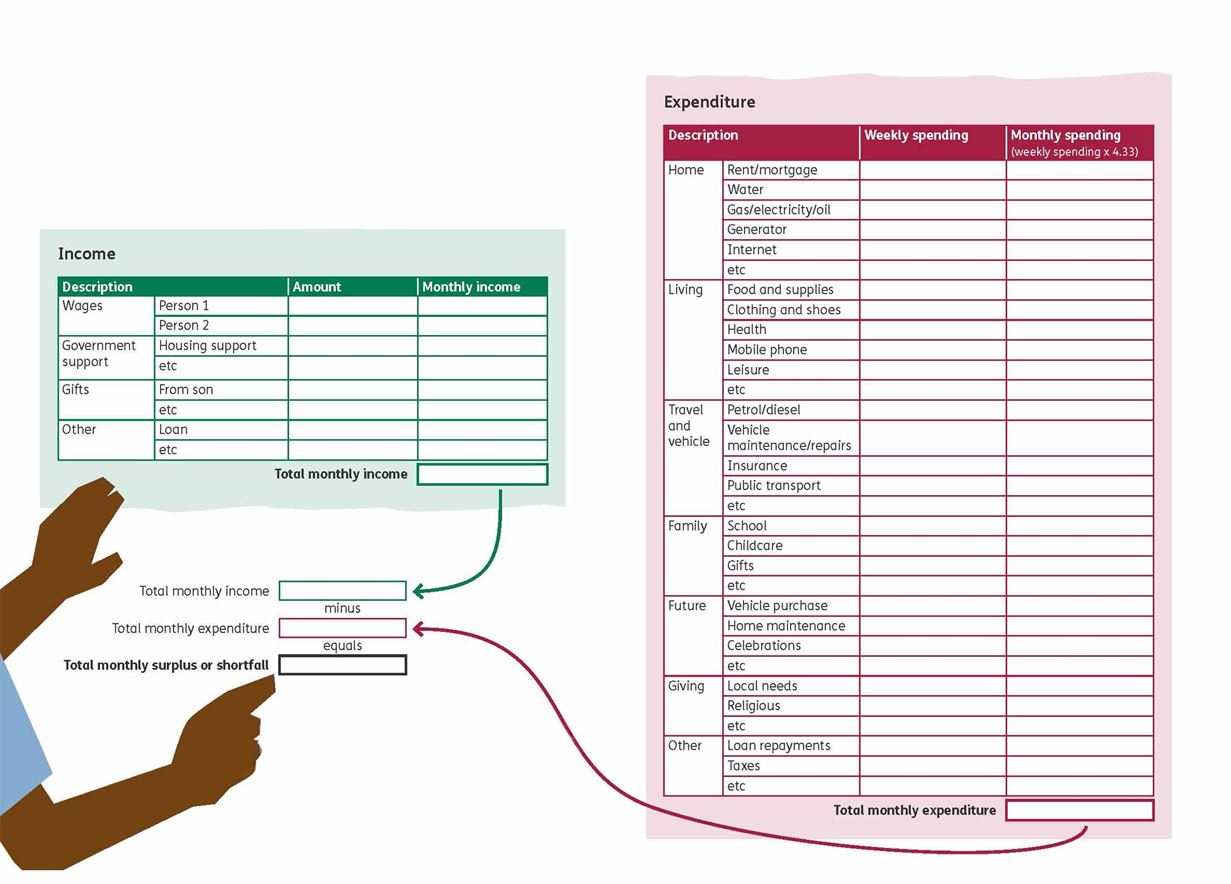

Three steps to creating a household budget

1. Income

Using a worksheet like the one on page 14, write down how much money you have coming in each month, including:

- wages (from your business or other employment)

- government support or pension payments

- gifts from friends and family

- any other income, such as loans from a savings and credit group

Remember to include any income that you might receive over the course of a year, but not necessarily every month. For irregular income, work out how much you receive in a year and divide it by 12 to get the monthly amount.